2024 Investment Themes

- Jan 25, 2024

- 10 min read

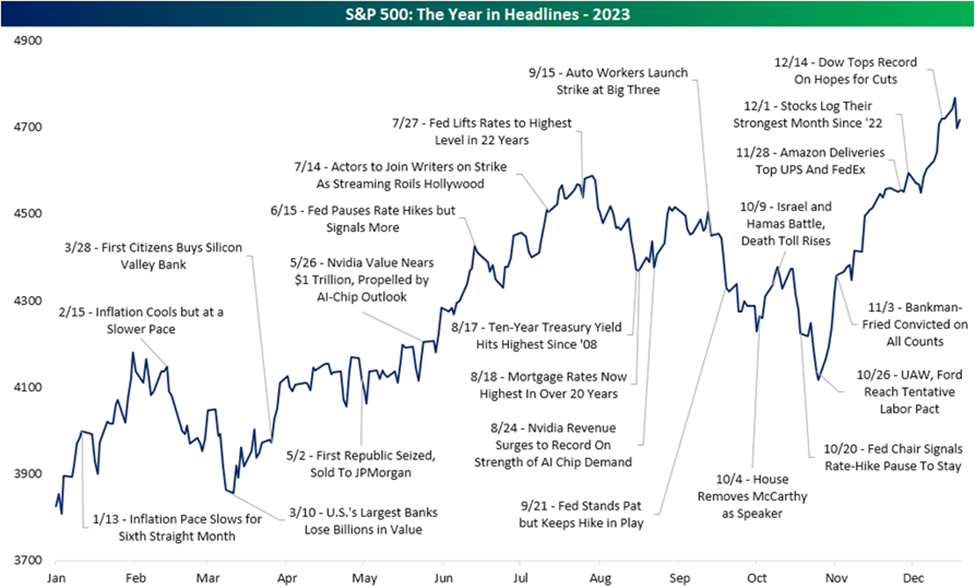

First and foremost, we would like to wish you and your families a happy New Year. Before diving into what we think will be the driving themes in 2024, please reference the below chart. As with every year, there was no shortage of surprises providing both volatility and opportunities.

January 2024

2023 In Review

2023 certainly delivered spectacular highs and excruciating lows in business with many unexpected twists and turns. We had a regional banking crisis started by Silicon Valley Bank which threatened to spark a run on all financial institutions. The Federal Reserve continued its inflation fight raising rates another 4 times in 2023. So far, it appears the Fed has potentially engineered an elusive soft-landing, but the debate still continues. Emerging markets had a banner year and crypto rose from the ashes after some eye-popping scandals. Nobody had a swifter fall than Sam Bankman-Fried, convicted for fraud and conspiracy and losing $16 billion in just days. Taylor Swift’s concert tour brought in as much money as the economies of some small countries, propelling her to the rarified status of music billionaire. And to top it all off, artificial intelligence ChatGPT entered all of our worlds.

When writing these updates, we always find it interesting to reflect on the past year’s events, which seemed like a big deal to the markets at the time. Reflection allows us to better understand how the markets reacted and subsequently how we and our clients responded. With this being an election year, we expect the level of hyperbole from our press core to increase significantly over the coming months. It always brings us back to the absolute truth of where returns are actually generated.

This is why we continue to repeat: know what you own, know why you own it, don’t try to control what you can’t and stick to your plan. Warren Buffet said it better when listing his rules to investing. "The first rule of an investment is don't lose [money]. And the second rule of an investment is don't forget the first rule. And that's all the rules there are." Now this has been taken too literally over the years as even Mr. Buffet isn’t a 100% batter. What he was trying to convey is that being forced to make up for large losses impacts compounding returns. The below illustration shows how average return is not the main metric to compounding your return on money. As you can see from portfolio B, avoiding large drawdowns led to a higher compounded return.

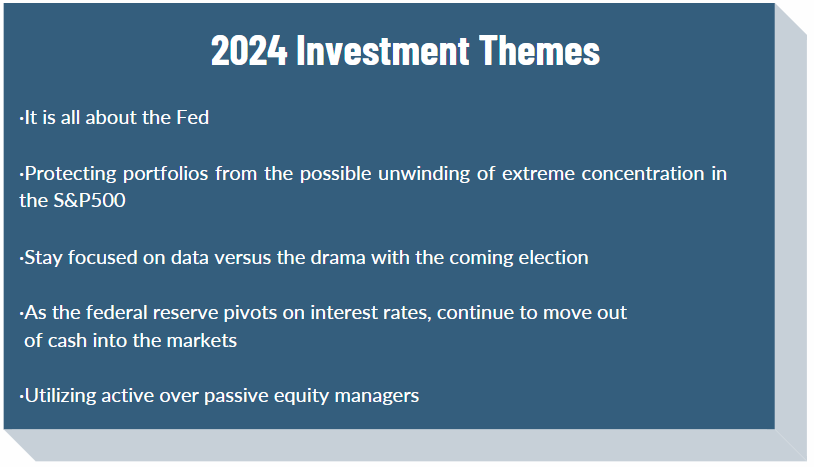

We realize some of our clients read our updates thoroughly and others just want the bullet points. For those of you who prefer to get to the punch line, we are listing our themes, which will guide our investment decisions. We hope you find the following information informative and useful.

Theme #1: It is all about the Fed

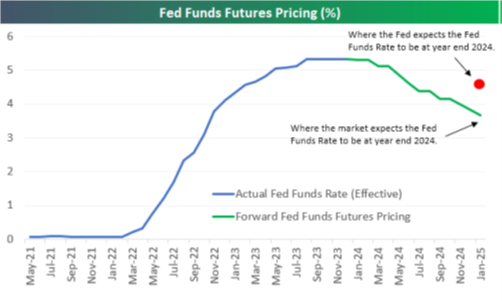

Don’t fight the Fed. As is usually the case, the Fed was behind the curve on inflation. While there’s optimism that they will nail the peak in inflation and ultimately cut rates at the right time, the burden of proof is on them. The Fed has signaled they will cut rates three times in 2024 while the market is pricing in six or seven cuts.

It’s important to remember that the Fed usually cuts for a reason, and market weakness following peaks in the Fed Funds rate isn’t uncommon. Even if the Fed does cut rates three times in 2024, the fed funds rate would end the year between 4.5% and 4.75%, still much higher than the virtually zero level of the past years. We believe they will stay restrictive until it tames inflation back to its 2% annual target, a job that it has yet to fully accomplish. While it's hard for the Fed to even predict what they will do down the road, markets see current rates as way too tight and are pricing six to seven 25 bps cuts in 2024. Additionally, current policy is historically restrictive, especially related to cooling inflation. Adjusting for inflation, the current Real Fed Funds rate is now well above the historical average. Breathing room for the Fed is coming from falling supply chain pressures, declining rental rates, growing residential supply, rising auto inventories and falling used vehicle values. Futures markets are pricing in 1.4% of Fed easing by the end of 2024. We currently think it will be less as the Fed is ultimately fearful of reigniting inflation. They can’t afford to get it wrong again.

The markets have incorrectly priced in a Fed pivot 7 times in the last two years. For the Fed to cut rates 6-7 times in 2024, we think you would need a global crisis or a deep recession with high unemployment.

The above shows the market does not always get it right, but we do believe the Fed has in fact begun to pivot and will begin to consider lowering rates in 2024. Regardless of how fast and the exact timing of when the Fed lowers rates, we like our positioning in high quality medium duration fixed income. The current yield above 6% continues to provide a nice cushion.

We expect the US equity rally to continue but look very different in the coming months. The continued strength in US equities is to some degree contingent on three factors:

1. Oil prices don’t spike.

2. Rates don’t continue to rise.

3. The dollar doesn’t meaningfully rally.

As the Fed’s message and path forward becomes apparent, we will adjust our models accordingly.

Theme #2: Protecting portfolios from the possible unwinding of extreme concentration in the S&P500

Impressively, just 5 stocks, or 1% of the index, accounted for more than half of the S&P's rally this year! Over the past couple of years, equity returns have been very concentrated. Since the Fed started to raise interest rates, shares in the biggest companies, which are largely the main tech stocks, have gone up around 25%. The market ex tech has gained 4% and the median stock is flat at 2%. When looking at the weighted index of the S&P500 the market doesn’t look cheap. However, the weighting of the “Magnificent 7” has really skewed multiples. The S&P 490 is much more reasonably valued, and small caps are cheap relative to large caps. There continue to be wide disparities in valuations based on market cap. When the market has become very concentrated in a few stocks, investors have historically done better by allocating away from those stocks. As we always shy away from “this time is different,” we are continuing to focus on managers who look different from the basic indexes.

We also think artificial intelligence (AI) will continue to be in focus. AI has captured investors' attention and contributed to the outperformance of the Magnificent 7 and technology stocks more broadly. We think its impact will broaden this year and be more about its adopters rather than creators. As companies increasingly focus their capital spending on productivity-enhancing investments related to AI, its impact will be felt across a spectrum of industries and sectors. The real question surrounding AI that remains to be answered; can the adopters of this innovative technology prove real economic value to justify these valuations?

Theme #3: Manage emotions during an election year

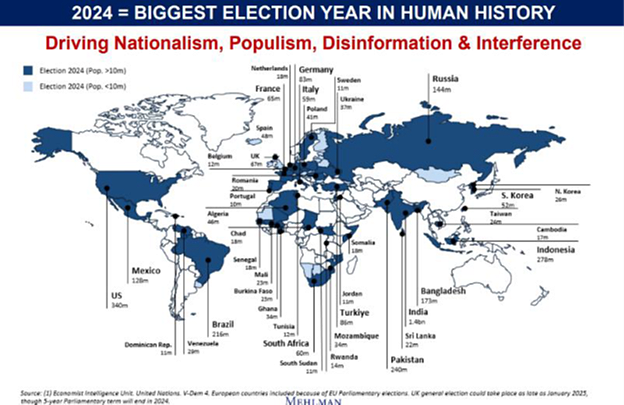

There will be an exceptional run of elections across the world during 2024 coinciding with a renewed interest in fiscal policy.

The year brings important elections in Mexico, Brazil, France, Germany, Italy, Poland, Turkey, South Africa, India, South Korea and more. Some 40 national elections are coming this year. A US election year highlights the partisan division threatening government’s ability to spend and has the potential to shift geopolitical goal posts meaningfully in both Europe and Asia. US presidential elections will introduce another wave of political uncertainty. The prior election highlighted the deep polarization of American politics, but history shows us the market is agnostic when it comes to political party.

On the whole, investors don’t appear to mind who wins elections, but they dislike the uncertainty and are glad to get them out of the way. In particular, close, hard-to-call elections tend to be followed by strong performance as uncertainty is removed. Rather than thinking about the economic or whole-market impact of the election, however, it has often been more productive to think in terms of sector effects. After all, relative performance within the market persists regardless of whether the whole market is going up or down.

There is also a pattern of volatility around elections as investors dislike uncertainty. Rotation between sectors and industries is common as the market digests the likely winning party. From the chart below you will see an increase in volatility 90 days prior to the election and stability returning over the following 6 months.

Theme #4: As the federal reserve pivots on interests rates, continue to move out of cash into the markets

Regardless of when and by how much the Fed lowers rates, money market funds are not a permanent or long-term investment. After years of an almost zero interest rate environment, making the current yield of around 5.35% on a money market fund feels great. However, having too much cash has an opportunity cost. Using last year as an example, the money market funds we used had a better performance than our taxable fixed income model for most of the year as we waited for the Fed to pivot. When they finally did, intermediate high-grade corporates solidly outperformed MMF. We think that lost opportunity cost could get more expensive this year as rates come down. When inline with our clients’ investment plan, we will continue to “lock” in these rates by transitioning out of heavy cash positions.

The years following a period of rising rates brought improved returns for stocks relative to cash. In referencing the chart below, equity returns significantly outperformed cash over the 12-month period following the end of the Federal Funds rate hike cycle. For fixed income, the main theme is locking in this income while we have it. It also sets up a potential for capital appreciation if a hard landing occurs, forcing the Fed to lower rates faster than anticipated.

With the yield curve still inverted, we continue to invest in the sweet spot with an intermediate duration. Staying too short using MMF will eventually have an opportunity cost when rates normalize. This also gives us potential upside if we get a hard landing scenario. If we use the index as an example and rates fall 1%, we could be getting a total return of 11% after appreciation and income. In the case where inflation moves higher and rates move up 1%, the higher coupon gives us a cushion where the index would only fall 1%. This scenario highlights the potential for a better risk/reward outcome by locking in more duration versus cash.

Theme #5: Utilizing active over passive equity managers

This one could be a sub bullet point to several of our prior themes. With the potential unwinding of historically high concentrations, an election year, and uncertainty around a hard/soft landing, utilizing active managers over passive indexes continues to make sense to us. We are agnostic in our belief on this subject, and believe different environments favor one over the other. Further oversight and management will be necessary when looking what we see as potential headline risks in 2024.

The market always climbs a wall of worry, and the yearly volatility is what creates the opportunities. With the current environment, we think active management is better suited for 2024 and improved potential for risk adjusted returns. As shown in the chart below, remaining invested throughout the year tends to yield the best results. Active management allows investors to better control their emotions throughout the highs and lows of a year.

As always, we appreciate the trust you have placed in us to deliver on your financial goals. We are available to discuss in further detail how this applies to your specific investment and financial plan. Please do not hesitate to reach out to us with any questions. Again, best wishes for a healthy, happy and prosperous New Year!

-Clarus Investment Committee

Disclosures & Disclaimers

The opinions in the preceding commentary are as of the date of publication, subject to change based on subsequent developments, and may not reflect the views of the firm. This material is not intended to be relied upon as a forecast, research, or investment advice regarding a particular investment or the markets in general. Nor is it intended to predict or depict performance of any investment. This document is prepared based on information Clarus Wealth Group, Inc. believes reliable; however, Clarus Wealth Group, Inc. does not warrant the accuracy and completeness of the information. Consult your financial advisor as to what investment strategy might be best for you.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review and investment strategy for his or her own situation before making any investment decisions.

Neither the information nor any opinion expressed herein constitutes an offer or an invitation to make an offer, to buy or sell any securities or other financial instrument or any derivative related to such securities or instruments (e.g., options, futures, warrants, and contracts for differences). This report is not intended to provide personal investment advice and it does not consider the specific investment objectives, financial situation and the particular needs of any specific person. Investors should seek financial advice regarding the appropriateness of investing in financial instruments and implementing investment strategies discussed or recommended in this report and should understand that statements regarding prospects may not be realized. Any decision to purchase or subscribe for securities in any offering must be based solely on existing public information on such security or the information in the prospectus or other offering document issued in connection with such offering, and not on this report. All opinions, projections and estimates constitute the judgment of the author(s) as of the date of the report and are subject to change without notice. Prices also are subject to change without notice. Clarus Wealth Group, Inc. is under no obligation to update this report.

Neither Clarus Wealth Group, Inc. or any employee of the firm accepts any liability whatsoever for any direct, indirect or consequential damages or losses arising from any use of this report or its contents. Examples and historical data contained herein are provided are for illustrative purposes only and not intended to be reflective of results you should expect to obtain. Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk and there can be no assurance that any specific investment will either be suitable or profitable for a client’s investment portfolio. You should not assume that any information presented herein would be appropriate in the future. Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income.

Some of the information is provided by Morningstar, Inc.; while these and other sources cited herein are believed to be reliable and assumed to be correct, readers are cautioned that accuracy cannot be and is not guaranteed.

More information is available by contacting Rex Whiteside, President, Clarus Wealth Group, Inc. He may be reached via email at Rex@ClarusWealthGroup.com or by telephone at 713-621-3500.

Sources: Sources: Bespoke, Apollo, Bloomberg, Capital group, Goldmn Sachs, JPM, Morgan Stanley, Schroeders,

Hambro, PIMCO, Brandywine, GWK, Vaughn Nelson, Fidelity, Schwab, Vanguard, Diamond Hill, Loomis

and others.